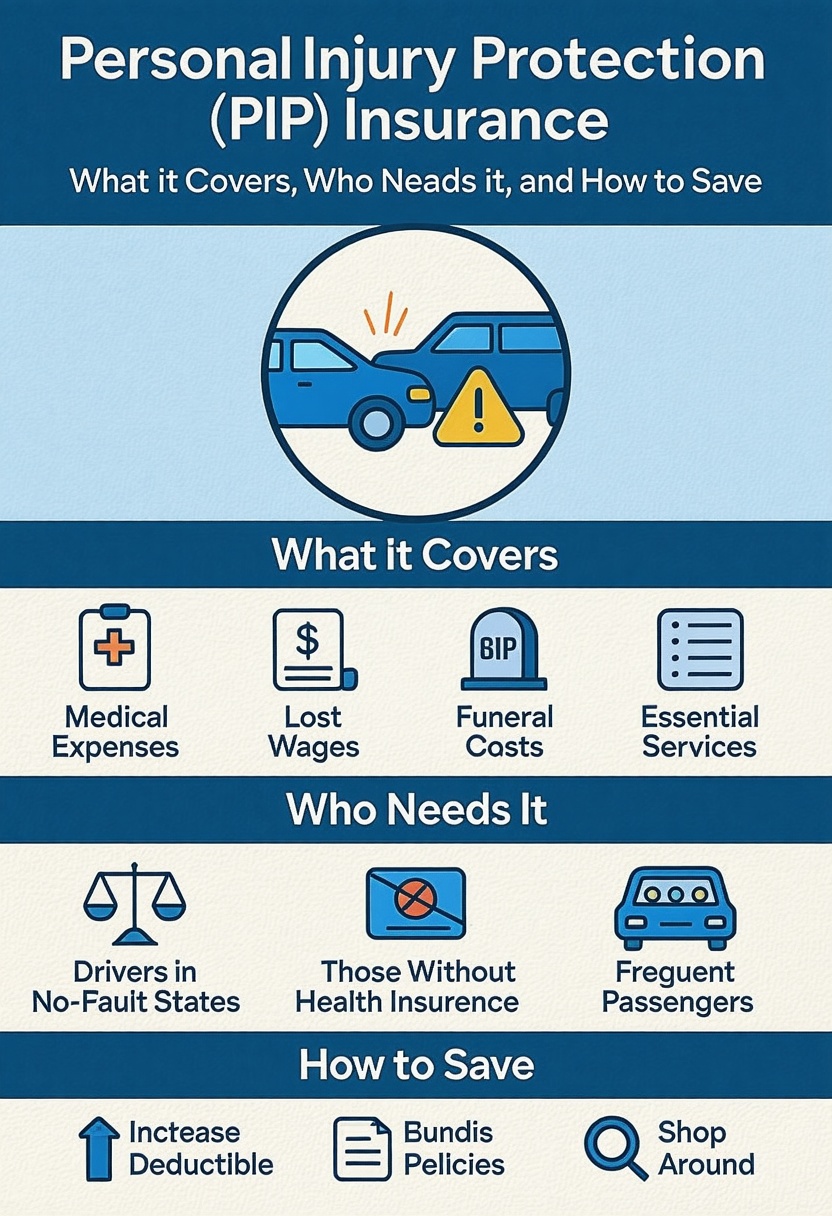

Understanding Personal Accident Insurance

In the unpredictable realm of life, accidents can happen to anyone, anywhere, and at any time. With escalating hospitalization costs and medical bills, it’s crucial to shield oneself with personal accident insurance (K1). This type of insurance can act as a financial safety net, offering much-needed support in times of distress. Moreover, the choice to extend this coverage voluntarily (K2) can provide additional layers of protection.

What is Personal Accident Insurance?

Personal accident insurance (K3) is a policy that provides compensation in the event of injuries, disability or death caused solely by accidental means. This form of insurance is particularly relevant to individuals who may be exposed to hazards in their occupation or daily life. It’s not just about insuring yourself, but also about ensuring peace of mind.

Many misconceptions surround personal accident insurance. It’s often confused with life or health insurance, but its scope and benefits differ significantly. Understanding these differences is critical to making an informed decision about your insurance needs.

Importance of General Accident Insurance

General accident insurance (K4) is a broader term that encompasses various types of accident insurance, including personal accident policies. It’s crucial to comprehend why such coverage plays a vital role in one’s financial planning.

In the event of an accident resulting in temporary or permanent disability, the burden can be overwhelming, both emotionally and financially. General accident insurance can step in to alleviate financial stress, allowing you to focus on recovery and rehabilitation.

Pros and Cons of Voluntary Accident Insurance

Voluntary accident insurance (K2) is an additional protective layer one can opt for, beyond the mandatory personal accident coverage. While this offers enhanced protection, it’s essential to weigh the pros and cons.

On the one hand, the voluntary nature allows for a more extensive range of benefits and larger coverage amounts. On the other hand, premiums for such enhanced protection can be higher, and the process to claim benefits may be more complex than with standard accident insurance policies.

Deep Dive into Voluntary Personal Accident Insurance

Opting into voluntary personal accident insurance (K5) allows individuals to tailor their coverage to their specific needs and circumstances, offering a sense of security in the face of life’s unpredictable events.

It provides a lump sum benefit for various situations, such as accidental death, permanent total disablement, or temporary total disablement. This financial aid can be an invaluable support during testing times, helping to cover anything from hospital bills to rehabilitation costs and loss of income.

However, it’s essential to read the fine print and understand your policy’s terms and conditions. Always remember that the goal of insurance is not only monetary compensation but also peace of mind in knowing that you can face life’s unforeseen challenges head-on.