How Much Does Urgent Care Cost? Real Numbers for Every Situation

If you’ve ever had a minor injury or sudden illness outside of your doctor’s office hours, you’ve probably wondered how much does urgent care cost before walking through the door. The range is wide, from around $100 at a simple walk-in clinic to several hundred dollars at a facility-affiliated urgent care. Knowing what drives the price helps you make a smarter choice. For comparison, the cost of an mri at a hospital can be ten times higher than the same scan at a freestanding center, and the same logic applies to urgent care.

Your insurance status is the biggest variable. With coverage, urgent care cost with insurance typically runs between $20 and $100 in copays, assuming the facility is in-network. Without insurance, the average urgent care cost for a standard visit falls between $100 and $200, though complex cases cost more. Knowing how this compares to emergency room cost without insurance, which frequently runs $1,000–$3,000 or more for even routine complaints, makes the case for choosing urgent care over the ER clearly.

What Affects Your Urgent Care Bill

The type of visit determines the base charge. A simple evaluation for a sore throat or minor cut typically falls in the lower price range. Adding tests like a rapid strep swab, urinalysis, or blood work increases the bill. X-rays at urgent care add $50–$200 depending on the facility. Each service is typically billed separately, so a visit that looks straightforward can add up faster than expected.

Facility ownership matters too. Hospital-owned urgent care clinics often bill at hospital rates, which include facility fees that independent urgent care centers don’t charge. Checking whether the urgent care you’re visiting is independent or hospital-affiliated before you go can be the difference between a $100 bill and a $400 one for the same level of service.

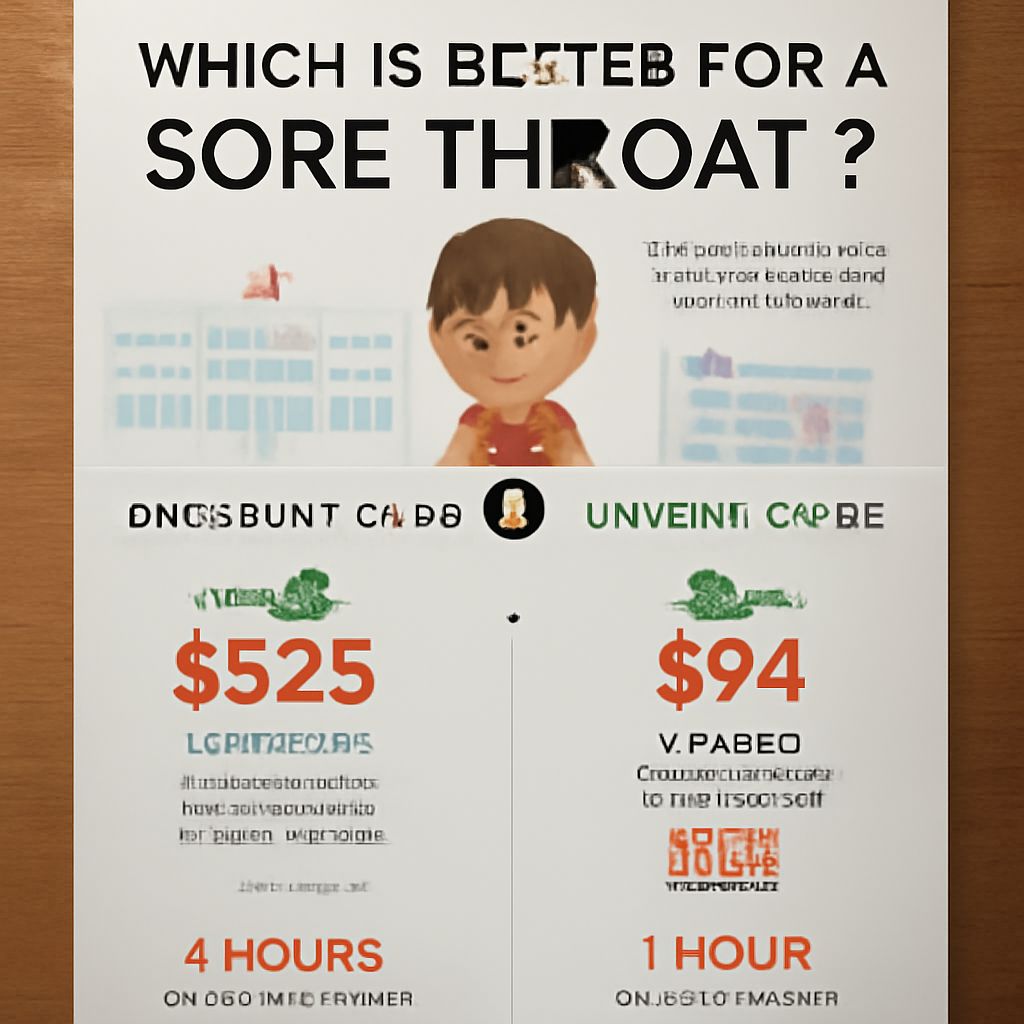

Urgent Care vs. ER: A Cost Comparison

The price difference between urgent care and the emergency room for non-life-threatening conditions is stark. An urgent care bill for a sprained ankle with X-rays might total $250–$400. The same visit to an ER could generate a bill of $1,500–$3,000 after facility fees, physician fees, and radiology charges. Emergency room charges without insurance are among the highest in the U.S. healthcare system, often leaving patients with bills they can’t pay.

Urgent care is appropriate for conditions like minor cuts, infections, mild asthma, sprains, minor burns, and flu symptoms. The ER is the right choice for chest pain, difficulty breathing, severe abdominal pain, signs of stroke, or any situation where delay could cause serious harm. Knowing the boundary saves both money and time.

Insurance, Copays, and Billing Surprises

When using insurance at urgent care, your copay is usually fixed, but that doesn’t mean it’s the only charge. If you haven’t met your deductible, you may owe the full contracted rate for services beyond the visit itself. Lab tests, X-rays, and medications dispensed on-site are often billed separately with their own cost-sharing rules.

Ask the front desk whether the facility is in-network for your specific plan before registering. Some plans distinguish between urgent care and primary care copay tiers, and choosing an in-network urgent care keeps your costs predictable. Out-of-network urgent care with insurance can result in much higher cost-sharing, sometimes approaching the out-of-pocket maximum for the visit alone.

Bottom Line

Urgent care is one of the most cost-effective options for non-emergency medical needs, particularly when you compare it to ER costs without insurance, which can be 10–20 times higher for the same condition. Calling ahead, confirming in-network status, and asking for an itemized bill after your visit are three practical steps that protect your wallet. If you’re uninsured, ask about self-pay discounts before services are rendered, as many clinics offer reduced rates that aren’t advertised.